Blog | 4/20/2020

COVID-19 and the Medtech Industry: Procedure Deferral Index

|

By Bridget D’Angelo, Engagement Manager; Mark Speers, Co-Founder and Managing Director; Susan Posner, Partner; Alena Petrella, Engagement Manager |

|---|

As COVID-19 has abruptly reduced non-urgent healthcare interventions, most medtech OEMs have seen their weekly sales drop over the last few weeks. Management teams are therefore eager to predict the degree to which their products will be impacted in the medium-term by the COVID-19 crisis and a likely recession. Health Advances has examined trends from the most recent recession and conducted a survey in the last week to anticipate how medical devices in various categories will be impacted. Fortunately, most categories will not permanently lose these product sales as COVID-19 has effectively created a backlog of patients who will quickly be rescheduled to receive treatments. However, since COVID-19 has triggered a recession, other product categories will, in fact, see slowed sales growth and/or sales declines during the recession.

Unlike the prior recession, COVID-19 has dramatically reduced non-COVID medical visits, diagnoses, and treatments as facilities put off all non-essential services in order to prioritize COVID patients, limit unnecessary supply usage, and reduce unnecessary exposure. In a Health Advances survey, administrators at ambulatory surgery centers (ASCs) and hospital outpatient departments (HOPDs) report that all elective surgeries have stopped, and the majority of semi-elective surgeries have also stopped.

Stay tuned for further detail in our upcoming blog post about COVID’s impact on the trend of shifting procedures to ambulatory surgery centers.

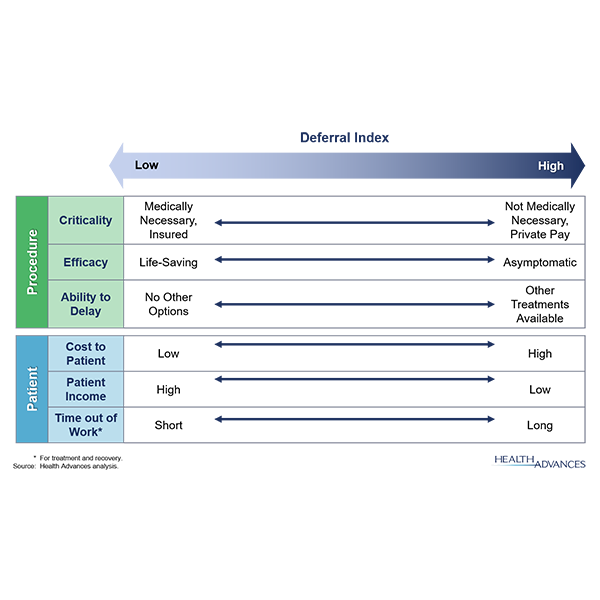

But what will happen to these procedures that have been delayed in an entirely unprecedented manner? How will volumes after COVID compare to before? Health Advances has compiled a list of criteria that determine a patient’s propensity to defer interventions to help estimate the behavior of each procedure type. The criteria include three factors related to the treatment itself: criticality, efficacy, and the ability to delay. In addition to these factors, patient-specific economic factors will also influence the propensity to defer: the cost to the patient, the patient’s income, and the time out of work needed for treatment and recovery. These criteria together form a deferral index:

Using these criteria, procedures can be generally grouped into categories as shown on the graphic below:

• The first is those that will continue regardless of COVID restrictions because they are deemed essential. These include any emergency procedures that cannot be postponed and are effectively recession-proof.

• The second category is acutely unique to COVID – procedures that normally would be considered necessary, but have been temporarily delayed. These procedures are likely to be performed in a bolus as soon as possible when restrictions subside. While the impact of this delay is difficult for patients and healthcare providers alike, medtech companies will recapture these sales within 6 months.

• The third category includes procedures which are not urgent but are ultimately necessary. These procedures (both those postponed already and those planned for the near future) are likely to be somewhat re-distributed over the next 12-18 months. This dynamic will result in a short-term decline for providers, facilities, and companies involved, but little long-term impact. The effect will likely be more pronounced for procedures that are primarily non-Medicare, as non-Medicare patients are more likely to lose their insurance as unemployment rises. However, we recognize that Medicare patients are also impacted by the out-of-pocket costs associated with a procedure and the recuperation period.

• The last category is those procedures commonly referred to as “self-pay” and are purely elective. While some postponed and scheduled procedures in this category will continue, many are likely to be postponed indefinitely and/or ultimately lost due to patients reprioritizing their budgets or opting for less expensive treatment alternatives.

A look back at procedure volumes during the last recession can help anticipate volumes in these categories. Kidney stone removal, for example, saw continued growth throughout the last recession as these procedures continued due to their acute nature. Because of the desire to keep these patients from COVID exposure, our survey respondents indicated that some of these procedures have been delayed, however, we expect an immediate rebound upon facilities re-opening.

Total joint replacements are considered “Deferred” procedures, where we expect a temporary slowdown in growth, but few long-term effects. The graph below shows the net sales of Zimmer’s reconstruction business, with a one-year dip in 2009 followed by growth more similar to pre-recession times. These procedures also benefit from being primarily Medicare procedures, reducing their vulnerability to unemployment.

|

"We believe the market for orthopedic procedure volumes temporarily decelerated on a global basis due to the weakened global economy…adverse conditions in the economy have resulted in a slowdown in elective hospital procedures. We saw evidence of recovery in 2009.” |

|---|

|

Please click here for further detail in our blog series about COVID’s impact on the musculoskeletal market. |

While some procedures may fall into the “Ongoing” or “Delayed” categories, certain technology options used in those procedures may be “Deferred.” For example, while procedures typically performed using robotic systems remained consistent throughout the last recession, Intuitive Surgical experienced a significant dip in robotic procedures as well as a flattening of placements, indicating that hospitals delayed capital investments and chose procedure approaches with lower supply costs. The Company has withdrawn its 2020 projections. However, it should be noted that this pause in capital investment was temporary, only lasting for a single year, even for such a large capital expenditure.

There are, of course, procedures that did not fare as well in the last recession. As an example, not only did LASIK suffer from lost patients in 2008-2010, but the timing of the recession permanently blunted the adoption curve of the technology so that volumes never fully recovered.

However, when certain elective procedures are deferred or abandoned, other less expensive treatment types often gain market share. While aesthetic laser procedures experienced a steep decline in the midst of the last recession and did not immediately recover, post-recession growth in aesthetic injections, a less expensive alternative, was strong.

Health Advances’ recent survey of ASC and HOPD administrators confirmed the re-distribution of procedures in these categories. These experts do expect most procedures to be rescheduled in the next 6-18 months, with the more essential and critical procedures first.

As medtech companies worldwide experience the unprecedented acute impacts from COVID, Health Advances is looking toward the future to better understand the medium- and long-term impacts of the likely recession that will follow it. In the graphic below, we outline key implications of each of the deferral index categories. The most intriguing insight for us is the fact that COVID is presenting an unusual opportunity for medtech companies to focus more on DTC marketing. Historically, when we have considered the cost:benefit ratio of DTC marketing for many products, the time from the treatment decision to the treatment has been too short to make DTC cost-effective. However, with the COVID-enforced increase in this timeline, many patients are awaiting procedures, are in their homes watching more television and doing more online searches than ever before. At a time when advertising rates have plummeted due to the decrease in advertising by consumer goods and services companies, there is a near-term opportunity to try to influence these patients to form brand preferences or consider alternative procedure options when given the time to conduct more research that they can bring to their physicians.

This post is part of a series of articles about the impact of COVID on various healthcare markets. Below is a summary of our findings across articles.

- COVID-19 has abruptly slowed many healthcare product markets temporarily, and it has triggered a recession which will impact our industry for longer

- While recessions lead to a deceleration in healthcare products markets, the effects vary significantly across markets

- In fact, when considering the clinical and economic factors unique to each market, many markets experience only modest and temporary declines

- Health Advances helps management teams anticipate the recession impact specific to their markets and suggests tactics to mitigate the impact while positioning themselves for subsequent growth

###

| About Health Advances Global MedTech Practice |

|---|

|

Health Advances MedTech Practice supports medical device executives evaluate and execute upon commercial opportunities, both organically and through M&A. We serve as a partner to medical device companies throughout the product lifecycle including identifying unmet needs, developing value propositions for new products, assessing market opportunities by segment, gaining market access at attractive value-based prices, and launching new products through direct sales and/or creative partnerships. If interested in more information, please contact one of the members of our MedTech Practice at medtech@healthadvances.com. |

| About the Authors |

|---|

|

Mark Speers is Co-Founder and Managing Director of Health Advances. Mark has been advising senior medtech executives for nearly 40 years. Susan Posner is a Partner at Health Advances and leader of the MedTech practice. Susan has over 20 years of health care industry experience. Bridget D’Angelo is an Engagement Manager at Health Advances, leading project teams for medical device companies and investors. Alena Petrella is an Engagement Manager at Health Advances, leading project teams for medical device and biopharma companies and investors. |